Closing and Post-Closing Services: What Is the Difference in Mortgage?

In the mortgage lifecycle, precision and timing are everything. From document preparation to final disbursement, every step must be coordinated seamlessly. Two of the most critical phases in this journey are closing and post-closing services. While they are closely connected, they serve very different purposes in ensuring a compliant, accurate, and fully funded loan.

For lenders, title companies, and servicing firms, understanding the difference between these two functions is essential to maintaining operational efficiency and delivering a smooth borrower experience.

What Are Closing Services in Mortgage?

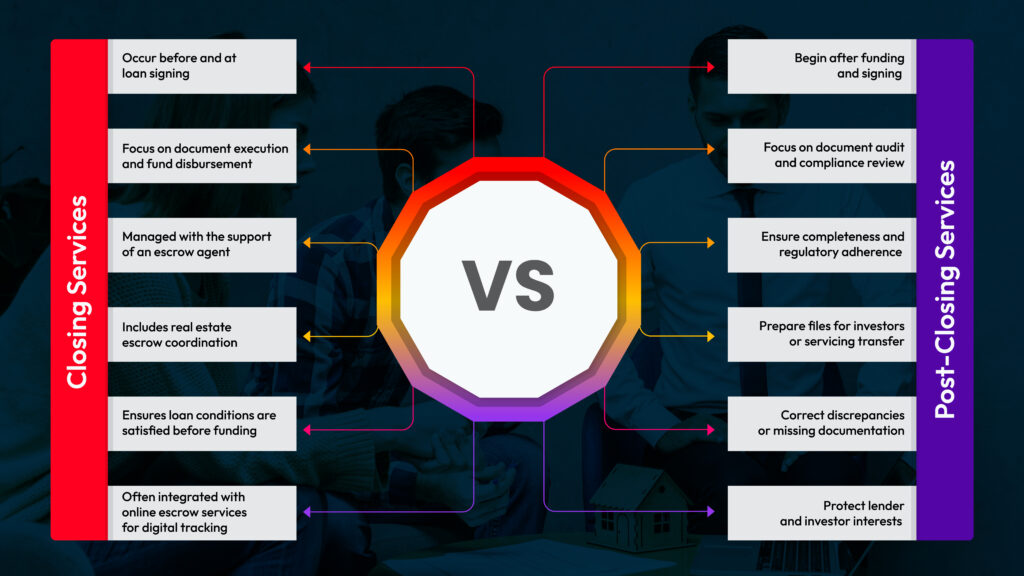

Closing services refer to all activities that occur just before and during the final signing of the loan documents. This is the stage where the mortgage transaction officially becomes binding.

At this phase, escrow services play a central role. An escrow agent acts as a neutral third party, ensuring that funds and documents are exchanged securely and only when all agreed-upon conditions are met. In real estate escrow, this includes verifying loan documents, coordinating signatures, collecting funds, managing payoffs, and preparing the settlement statement.

Escrow support teams assist with document preparation, compliance checks, communication with borrowers, lenders, and title companies, and ensuring that all closing conditions are satisfied before disbursement. With the growing adoption of online escrow services, many of these processes are now managed digitally, improving speed, transparency, and tracking.

The primary goal of closing services is simple: ensure that the loan is properly executed, funded, and recorded without errors or delays.

What Are Post-Closing Services?

Once the borrower signs and funds are disbursed, the work is not over. Post-closing services begin immediately after the transaction is completed.

Post-closing involves reviewing all signed documents to confirm accuracy, completeness, and compliance with investor and regulatory guidelines. This stage includes auditing loan files, correcting discrepancies, preparing collateral packages, coordinating document recording, and transferring files to investors or servicing departments.

If errors are discovered during review, post-closing teams initiate corrective actions. These may involve re-executing documents, updating disclosures, or resolving missing signatures. Strong escrow support during post-closing ensures that any gaps from the closing phase are identified and addressed before the loan moves forward in the secondary market.

In short, post-closing safeguards the lender’s investment and ensures that the loan file is fully compliant and sale-ready.

Closing vs. Post-Closing: Key Differences

Why Both Phases Matter

Both closing and post-closing services are critical to maintaining loan integrity. Weakness in either phase can lead to compliance violations, delayed investor purchases, financial penalties, or borrower dissatisfaction.

Efficient escrow services during closing help prevent last-minute surprises. Meanwhile, structured post-closing processes ensure that the loan file stands up to audits and investor scrutiny.

In today’s fast-paced mortgage environment, lenders increasingly rely on technology-driven escrow support and online escrow services to reduce turnaround times and improve accuracy. However, technology alone is not enough. Experienced teams are required to manage document flow, regulatory compliance, and coordination across multiple stakeholders.

The Invisia Advantage

At Invisia BPO, we understand that mortgage operations demand accuracy, scalability, and strict compliance. Our closing and post-closing support solutions are designed to streamline real estate escrow workflows, strengthen escrow support processes, and reduce operational bottlenecks.

By combining domain expertise with structured quality control, we help lenders, title companies, and servicing firms minimize risk while improving turnaround times.

Understanding the difference between closing and post-closing services is the first step. Optimizing both is what drives long-term success in mortgage operations.