Intelligent Process Automation vs RPA: Which Should You Pick

The real estate and lending ecosystem is evolving fast. So are fraud tactics. Over the last few years, title fraud has moved from being a rare risk to a growing operational concern for lenders, title companies, and mortgage servicers. Fraudsters are exploiting process gaps, outdated verification systems, and overloaded internal teams. The result? Increased exposure to mortgage fraud, title theft, and complex property fraud schemes that can derail transactions and damage reputations.

In this environment, automation is no longer optional. But the big question remains: should you rely on Robotic Process Automation, or is Intelligent Process Automation the smarter choice?

Before answering that, it is important to understand the risk landscape.

The Rising Threat of Title Fraud

Title fraud happens when a fraudster illegally transfers ownership of a property or forges documents to secure loans against it. In many cases, homeowners are unaware until a lender initiates foreclosure or collection proceedings. This form of property fraud is particularly dangerous because it exploits administrative weaknesses in document validation and title verification workflows.

For lenders, the impact is significant. Losses from fraudulent mortgages, regulatory scrutiny, reputational damage, and increased compliance costs are all real risks. Traditional safeguards are often reactive. By the time discrepancies surface, the financial and legal implications are already in motion.

This is where technology and structured outsourcing become critical pillars of title fraud prevention.

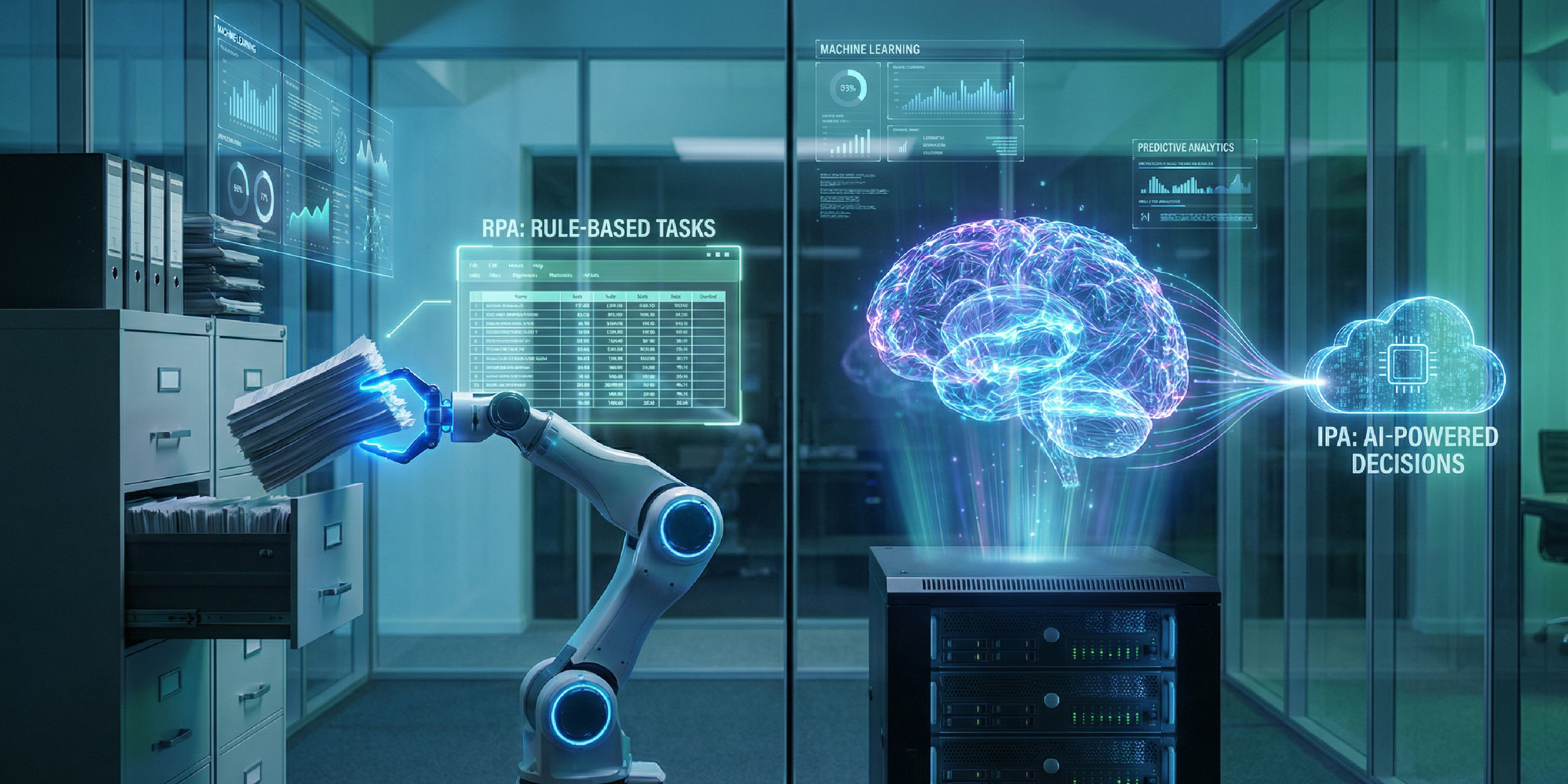

What Is RPA?

Robotic Process Automation uses rule-based bots to automate repetitive, structured tasks. In a lending or title environment, RPA can:

- Extract borrower data from forms

- Validate predefined fields against internal databases

- Trigger alerts based on fixed rules

- Generate standard reports

RPA works best when processes are predictable and follow strict rule sets. It improves speed and reduces manual effort. However, when fraud schemes become more sophisticated, rigid rule-based systems can struggle to detect anomalies that fall outside predefined conditions.

For example, a forged deed that looks legitimate but contains subtle inconsistencies may bypass basic automation checks if those inconsistencies were not programmed into the rule engine.

What Is IPA?

Intelligent Process Automation goes a step further. It combines RPA with artificial intelligence, machine learning, and advanced analytics. Instead of only following rules, it can analyze patterns, detect irregularities, and learn from historical fraud cases.

In the context of title fraud, Intelligent Process Automation can:

- Identify unusual ownership transfer patterns

- Flag inconsistencies in property history records

- Cross-reference multiple public databases in real time

- Detect behavioral anomalies linked to mortgage fraud

This approach supports proactive title fraud prevention rather than reactive damage control. It strengthens due diligence without slowing down the loan cycle.

RPA vs Intelligent Process Automation: Which Should You Pick?

If your goal is operational efficiency alone, RPA can deliver measurable benefits. It reduces turnaround time, improves document handling, and eliminates repetitive manual tasks.

However, if your goal includes risk mitigation, compliance assurance, and proactive title fraud prevention, IPA provides a more comprehensive shield. Fraud tactics evolve. Static rules do not.

For lenders handling high transaction volumes, relying only on RPA may create blind spots. Intelligent automation, supported by experienced outsourcing teams, creates a layered defense system. Human expertise combined with AI-driven anomaly detection significantly lowers exposure to title theft and property fraud.

Why Outsourcing Matters?

Technology alone cannot solve fraud risk. The effectiveness of any automation model depends on process design, monitoring, and compliance governance. Partnering with Invisia ensures:

- Continuous process auditing

- Updated fraud detection protocols

- Regulatory compliance alignment

- Skilled document examiners and analysts

A structured outsourcing model strengthens both RPA and Intelligent Process Automation implementations. It ensures the tools are not just deployed, but strategically managed.

The Final Word

Title fraud is no longer an isolated threat. It is an evolving challenge affecting lenders nationwide. Choosing between RPA and Intelligent Process Automation is not just a technology decision. It is a risk management strategy.

For organizations seeking long-term protection against mortgage fraud and property fraud, Intelligent Process Automation supported by expert outsourcing delivers a smarter, future-ready approach.

Ready to strengthen your fraud prevention strategy? Let’s connect and explore how Intelligent Process Automation can safeguard your lending operations.